Speaker 0 00:00:02 <inaudible>

Speaker 1 00:00:08 What's up, everyone. Welcome to the finance for physicians podcast. I'm your host, Daniel Raimi. Join me as we dig into what it looks like for physicians to begin using their finances as a tool to live better lives. You can learn more about our

[email protected] let's, jump into lays up. So what's up guys. Hope you're having a great day, uh, happy new year. It's, uh, early in January. And as we're recording this, so hope you're having a great year today. I was planning to talk student loans and PSLF or public service loan forgiveness. I think my goal here is to make sure you're not leaving dollars on the table. What prompted me to go down this path? I was talking with a buddy the other day and he is in academic medicine position and practice and was sharing that he's aggressively paying off his student loans, his federal student loans.

Speaker 1 00:01:02 And I was asking him about PSLF and if he was going that route and he was sharing how he felt that his income was at a level, that there was not going to be any value there anymore. And so in my head, I'm thinking, you know, is this the best strategy for him now? Just to clarify, we don't work with him in our planning firms. So I don't know his financial situation, so I'm not, you know, he could be doing the going the perfect route already, but putting my planner hat on, I immediately start thinking that, you know, is this the best strategy is the, you know, potentially missing opportunity with PSLF. And the reason, part of the reason my mind goes that direction in our planning firm, we've had the opportunity to see people's finances. And so we regularly see, uh, people kind of starting out down this road and it's probably one of the most common things we see where people are leaving quite a bit of money on the table.

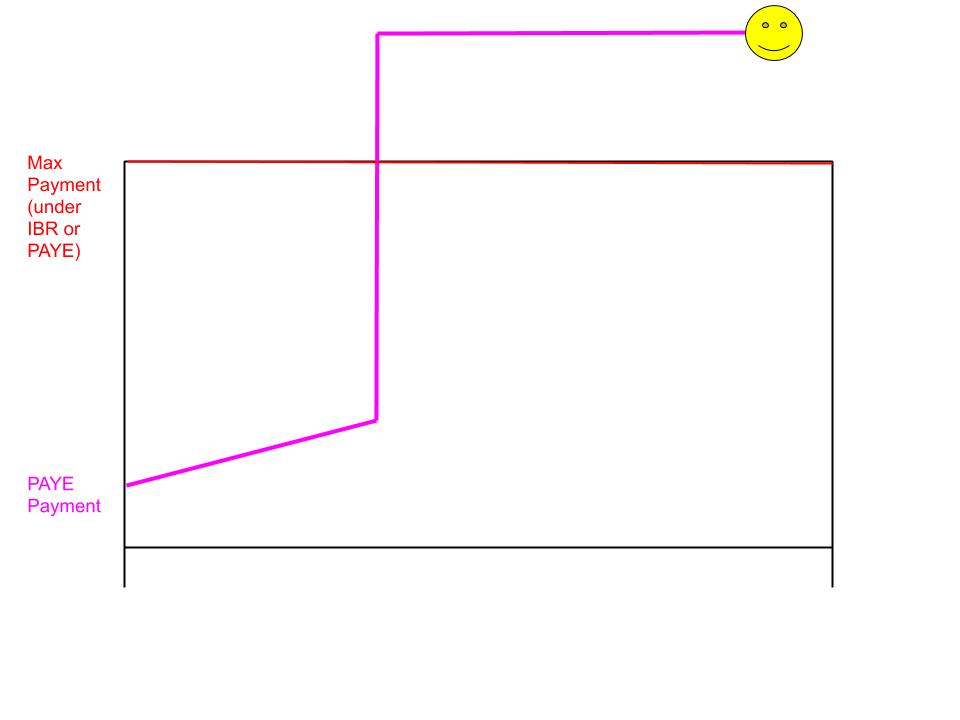

Speaker 1 00:01:55 That's the main reason I wanted to talk about this today is to really just to clarify what the big issues are. We see talk about some strategies to avoid those issues and ultimately help you avoid, uh, leaving dollars on the table with those federal loans. So if you have federal student loans, you're definitely going to get benefit out of conversation today. So I thought it would be helpful to talk through several scenarios and we can kind of just explore some of these concepts and, and look at the, you know, how it works in these given scenarios. And then talk through that. So this first image, if you're watching the video, you'll see the image, but I'll share the, uh, the images on the show notes, but I'll kind of talk through these in case you're not able to see these, but the first concept is meant to kind of illustrate what I think maybe my, my buddy has, has been doing.

Speaker 1 00:02:50 So, you know, when you're in training, your payment is typically going to be very low for federal student loans. If you're any income-based repayment plan, it's going to be, you know, low because it's a percentage of income. And so in this example, I'm using pay or pay as you earn. That's one of the income-based repayment plans and showing that low payment in training. And so there comes a point, you know, you go into practice and the income jumps up quite a bit. And so at the same time, the payment's going to go up on your federal student loans. And so if you're like my buddy and you're like thinking, okay, I just want to get rid of these things, pay them off as fast as I can. I don't think there's any PSLs benefit you're going to just basically pay as much as you can.

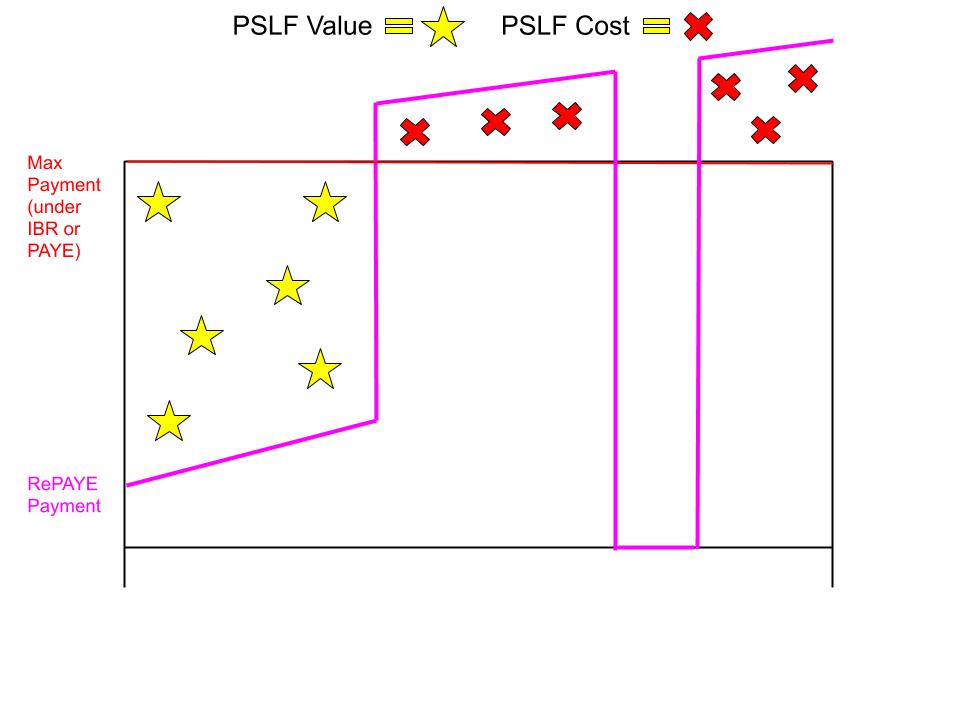

Speaker 1 00:03:42 And so payment jumps up a lot and you pay as much as, as you can and pay it off as fast as you can. And then at the end, you know, you get smiley face, it's all gone. What'd you see here, there's something to clarify with, uh, income-based repayment plans. Uh, well, two of the income-based repayment plans, IBR and payee both have a max payment. So that's meant to be this red line. So there's a ceiling that you don't ever have to go above. I mean, you can always choose to pay more than that, but there's always going to be a ceiling that you don't, you would never have to go above on pay and IBR and that's ceiling gets set at the beginning of repayment. So, you know, at this beginning stage, when you're starting your repayment plan, they're going to set this max ceiling.

Speaker 1 00:04:36 And basically all it is is they look at the balance at that point in time and they just calculate, you know, how much would you have to pay to pay the thing off in exactly 10 years? And that's really all it is. So that's, that's where that max payment comes from all circled back to that. But that's very important if you're in payee or IBR, but what happens is if you're paying at this lower level in training and you transition into practice, if you do want to pay it off in any amount of time, you know, sooner, 10 years or sooner, you're going to have to pay quite a bit more than that max payment you would have otherwise had to pay, you know, in that high income scenario. So that's kind of where we'll say that, that situation where my buddy is, is he painted off as fast as possible.

Speaker 1 00:05:22 Now I'll throw out an, uh, another scenario just to kind of clarify this. What I have found is a lot of people don't even don't realize that they are actually even qualified in the first place. They don't realize their employer is actually qualified. So that's, that's not my buddy's situation, but I, I see that happen in every once in a while is people are just paying off their federal loans as fast as they can, because they don't even realize that their employer might qualify for public service loan forgiveness. And so that's kind of another issue I see. And so you want to make sure that, you know, for certain that your employer is, is, or is not qualified for PSLF, it's basically going to be, you know, five Oh one C, three non-profits and government employers are the obvious ones. So you can, should be able to easily find that out by looking up, you know, there's a five Oh one C3 search tool.

Speaker 1 00:06:17 You can use employer identification, identification numbers, which are on your W2's and you should be able to ask for that. You should be able to look that up pretty easily, um, government employer, or a five Oh one C3. Now there's another category of non five Oh one C3 nonprofits. There are a little harder to look up and verify, uh, but you should be able to, you just need to ask around and get someone that can, can verify that. So you want to, um, make sure you're not just failing to understand that your employer is actually qualified for PSLs in the first place, but the remainder of this will assume that you are in fact qualified and we'll kind of talk through what that might look like. So I think the other important concept is to really understand, uh, how the PSLF program works or where the value originates.

Speaker 1 00:07:09 It's really counterintuitive because you think of a debt and you're like, okay, I got to pay the debt off. And there's a payment schedule and you know, there's no free money. Really. It's just a matter of, uh, you know, what is the interest rate, but with PSLF, it's completely not that away. There, there is plenty of value to be had, uh, from this forgiveness event. And so basically the concept is you must make these qualified payments 120 of them, and it doesn't actually matter how much you pay each month. You could be paying zero, actually, you know, if your income's well enough, you're paying zero. Or if it's COVID forbearance, you're paying zero. So as long as you are, uh, you know, making that payment, no matter what it is at the end of 120 of them, it gets forgiven. Doesn't matter what your balance is.

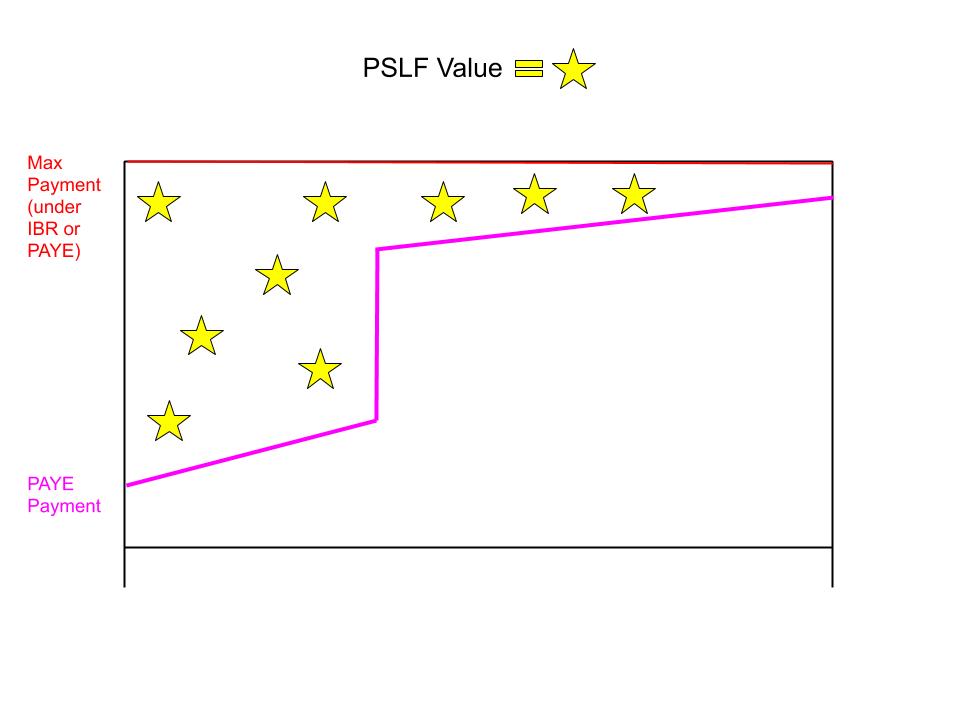

Speaker 1 00:07:59 That actually is irrelevant and there's no tax impact whatsoever. So literally it's a payment plan and that's it. And it is not, it's driven more on your income and not actually the balance. And so what happens is, so going back to that max payment concept. So at the beginning of your repayment plan, there's this max payment that's going to be set that's a 10 year schedule, what you would have otherwise had to pay to pay it off in 10 years. But in reality, in training, you're going to be paying a lot less than that because it's a percentage of your income. And so in the example, we're looking at now, the payee payment is, you know, low. Like I was just talking about, uh, maybe it increases a little bit, but it's relatively low. Uh, and then it jumps up in practice, goes up. And then in this example, we're looking at here, I'm assuming your, uh, income based payment.

Speaker 1 00:09:00 So if you stick on the income-based repayment plan, pay ye if you stick with payee and in practice, let's say, based on your income, your payment is still a little below this max payment calculation. And that continues to the end of the 10 years. So that's the scenario. Your payment is really low in payee and training. It jumps up quite a bit because your income goes up, but it's still a little below the max from then until you get to the 10 year Mark or 120 payments. So where's the PSL of value come from really the easiest way to look at it is it's everything below that payment ceiling, all that, the difference between each payment, actual payment and what the 10 year payment would have been, or the payment ceiling is, is all value. That's all, you know, essentially free money, uh, because you would've had to pay that max payment, if you were going to pay it off in 10 years in a normal debt scenario.

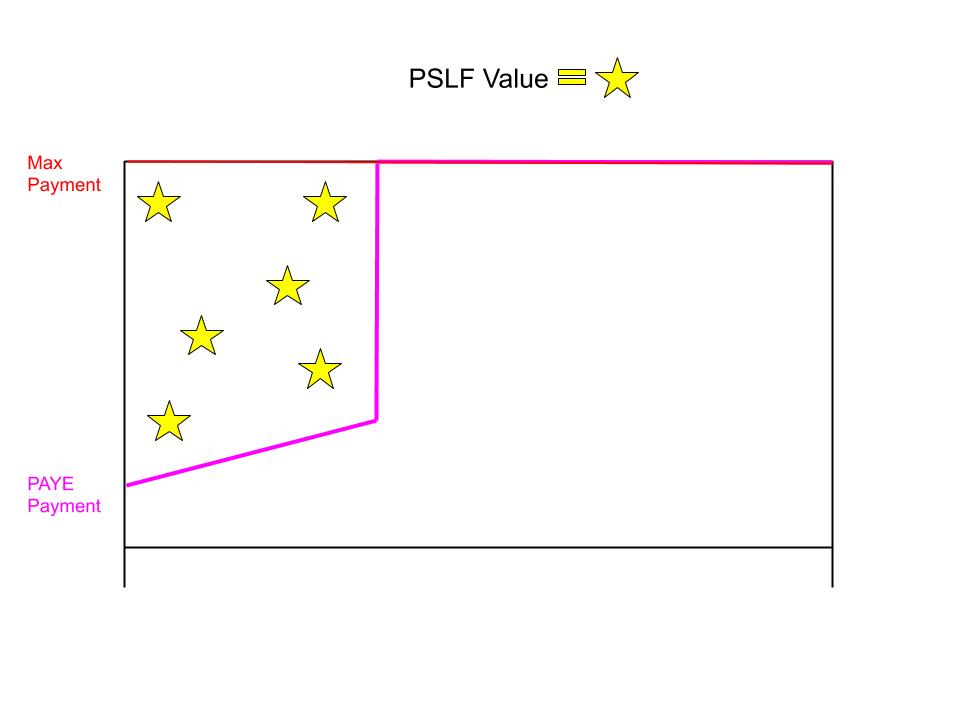

Speaker 1 00:10:02 And in re you're actually only having to pay this payee payment. And so this number can be substantial, like very, very large, particularly because of this training period, because it's so low. Another misconception about this switch in the into practice is that a lot of people don't realize that the payment calculation is based on AGI from the prior year. And so there's kind of a lag, uh, it takes a while to catch up. So that's, that's that kind of adds considerable value here in this transition phase, because with PSLF remember the lower you pay, it's always, you know, the lower you pay, the more value you get. So this is the scenario where your payment does not ever cap out in this payee example, but, um, you know, I'm going to, for my buddy's example, I'm just gonna assume, uh, he, his income was at a level where he capped out.

Speaker 1 00:11:01 Um, and so let's say he's, you know, in practice for a while and he's at this cap payment. So that's, I think where the, some of the misconception can come from is like, Oh, well, I'm capped out. I'm I'm at the max income. The value is not there. The problem with that is there still would be substantial value, even if you've already capped out, mainly from those payments and training. That's where the bulk of the value is as, as it is. And so it's like you have to pay the 10 year payment, really only the 10 year payment for say six years. And you know, this much lower payment for four years. So all that is free money. So that's still like a home run potential deal there. Now, there, there, there are a few situations where, you know, for example, if you're in training and you make no payments for like forbearance or deferment, and you're kind of like starting out at the max payment, that's, you know, going to be an issue cause there's no value to be had.

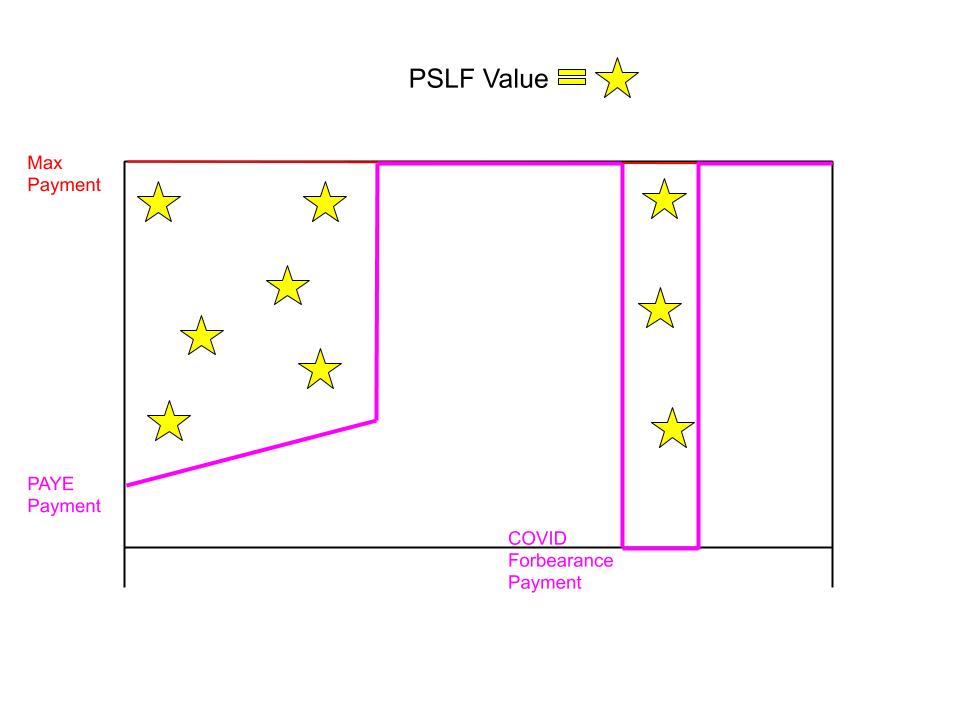

Speaker 1 00:11:59 So you really have to look at how far below this actual payment line am I with my, uh, income-based payment. The other thing that has happened lately has been COVID forbearance. So that's, that's kind of a nother huge, um, really a huge benefit for people, especially people that were at that max payment. So with COVID forbearance, you're, you're only required, well, you're not required to make any payments. There's no interest being charged and all those $0 payments are still qualifying for PSLF. So that adds tremendous value. That's we're up to 11 months. Some people say a lot of people say it's going to get extended again, but the longer that is the more value there is, but basically you're getting all this value from the difference in your, you know, max, your ten-year cap payment and the actual COVID payment, which is zero, that's all value, you know, PSLs value in your pocket.

Speaker 1 00:12:59 In, in that situation. There's also some, some opportunities. So once you kind of understand how this PSLs system works, you start to look at it and you're like, okay, well, the concept is less, is more the less, the lower my payment, the more value I get. And so if that's the case, well, what are they, how do they define income? Well, the answer is adjusted gross income. And so what is adjusted gross income adjusted, gross income. Actually, you can kind of do some things to strategize and potentially lower that number. So there's some strategy that you can utilize to kind of further pull that payment down. So I'll throw out some examples. Uh, there would be the retirement plan example you put into pretax retirement plans like four, three, B, or four 57 or whatever, uh, or you do an HSA, which is pre-tax or put in you, you pay health insurance premiums.

Speaker 1 00:13:54 Those are all pre-tax things that come out of payroll, typically that lower your AGI and allow your payment to be less. Another common example we see is filing taxes separately. That's a way to exclude spousal income and further pull this line down for your situation. But the gist of it is there's a lot of different strategies to implement that will continue to pull this payment down. So that that increases the PSLF value here. Now, there are going to be situations where I already hit on a few, but there's, there's going to be situations where, you know, given all this, it still doesn't work to go for PSLs, even though you're in a qualifying employer set up there, they're pretty rare in my experience, but they do exist. So repay Yi is one example when income is at a high enough level. Now, quick side note on that before I explain how this works, you can switch out of repay into payee or IBR as long as your income is low enough.

Speaker 1 00:15:02 So as long as you do it before you hit this cap, uh, as long as you do it, before income goes above some certain level, you can switch out of repay and get into a pay your IBR so that you have a max payment cap. The problem with repay is there is no max payment caps. So if your income goes high enough, you're going to exceed that whether you want to or not. And so going back to the first example I gave, where you start in training and payment is low, repay looks very similar to payee, and then you transition into practice. In this example, let's say the income is very high as a percentage of the debt. And so you actually exceed that max payment, you would otherwise have paid under payee or IBR, and you keep paying at that level. And so that kind of like reduces the value of PSLF cause you're now kind of paying more than you would have otherwise paid.

Speaker 1 00:15:59 Now you could have this COVID COVID forbearance situation that comes into play that kind of adds further value. And then you bounce back up to a higher payment. But the gist of it is you want to start to understand all these factors and really the key is to run the numbers and, you know, look at your situation and see, you know, exactly what the cost is of the PSLs situation and compare it to what the cost would be in the, I pay it off as fast as possible scenario. And then you can even incorporate, you know, if it's close or if you're starting to see there is some PSLs value, you can incorporate some of these strategies to try and reduce, uh, income, which will reduce payments and maximize that PSLs benefit. So I think if we're summing up all this, if you're thinking, okay, you know, that's, that kind of makes sense, but, uh, what, what do I do?

Speaker 1 00:16:55 What can I do today? And so what I would suggest is for starters, just everyone should make sure their current employer is verified or not. If there's any question, um, make sure your current employers is qualified for public service loan forgiveness, and you should be able to do that. If they're a five Oh one C three, you can find their employer identification number and search for that online, we can link to some, uh, uh, five Oh one C3 search tools. And if it's a government employer that should be straightforward as well. Now, if it's the gray area, nonprofit on five Oh one C3, it might be a little more, more tricky, but, um, you should be able to find someone and get them to verify whether or not they are a qualifying employer. I would also encourage thinking about future employers and, you know, see if the type of setup you're going to be in, might be qualifying as far as an employment situation you want to, I think it's good to be flexible.

Speaker 1 00:17:57 I can't tell you how many times people have come to me and said, I was totally not planning for PSLs and surprise. I end up in this job that is qualified. And so what do I do now? So you don't want to, um, you gotta be careful, you know, assuming too much about your future. The other big thing is making sure your, your actual loans themselves qualify. Now, this is not as common of an issue as it used to be, but, uh, there are some types of loans that are not qualified for PSLF. The key is look for direct. The word direct is key. So if your loans are FFL, those do not qualify. You want to look to make sure your loans are direct Stafford or direct flaws or whatever, just to make sure those qualify. There are steps to if they do not qualify to get them qualified, but we'll save that for another day.

Speaker 1 00:18:52 The other big thing is understanding where you stand, you know, to run the numbers. You have to understand how many payments you already have and see kind of where you're at on this chart and the best way to do that. Well, you can look at your kind of history and add those up, but ultimately the best way to do that is to submit employer verifications for prior employment periods. And you can send those into your loan servicer, and they will give you kind of a count as to how many payments you have as of that point. And you can use that to say, okay, of the one 20, how many do I have so far? And then you can use, start there and push the numbers forward and say, okay, what's my total looking like, and then really it comes down to, you know, once you get, get all your current information organized, you just want to run the numbers and compare what's your PSLF strategy or PSLs scenario would look like and compare that to, you know, what you're doing now.

Speaker 1 00:19:51 And maybe even, you know, of consider some of the strategies I mentioned, you know, maybe minimizing AGI or filing separately on taxes, or even changing repayment plans. Like you can switch in certain cases. So you want to consider those strategies. So once you've gone through all of those strategies and you have kind of all your numbers laid out there and you've, you've run the numbers and you, you understand kind of exactly what it looks like for your situation. If at that point, PSLs still does not look beneficial. Then at that point, you definitely want to consider a private refinance because in this scenario where PSLF is of no value, you're going to have to pay back the entire balance. And so interest rates become critical at that point. And with interest rates. Now, the federal loans are going to be higher in most cases than a private refinance.

Speaker 1 00:20:48 So, you know, the average federal loan might be 6%, sometimes seven, sometimes even 8% interest rate. And with private loans, if you have really good credit, especially, uh, we see people with, uh, interest rates as low as 2%. Now that's on a five-year variable type of example, but you can see, you know, five year fixed periods, uh, maybe in the two and a half, 3% range. And so 3% is considerably better obviously than a 7%. So that's, if you're going to have to pay off the entire balance, either way, you're going to save considerably on the interest savings, but you want to be careful not to do that before, you know, checking off the check box that PSLF is for certain not of value. The thing is with, with, uh, PSLs it's, it's gotten pretty complicated, especially when you are in practice and married. And, and particularly if you have two people with federal student loans, there's plenty of people that will have kind of, this'll be like your head's spinning after, after hearing all this.

Speaker 1 00:21:53 And so if you have questions on it, feel free to reach out to us. We're happy to answer questions. We can also cover them in future future shows and whatnot. And if you need kind of more full hands-on service, help, definitely reach out to our planning firm and financial. Uh, that's, that's what we do. The main thing though, is we want to make sure you're not leaving money on the table. And really that comes down to just educating yourself, understanding how it works and getting the numbers, running the numbers and understanding what those look like so that you can make a solid, educated decision. Hope that's been helpful. Look forward to catching up again next time. And, uh, y'all have a great day

Speaker 2 00:22:31 As always. Thank you so much for joining us today. If you found this valuable, please give us a review on iTunes and share with a friend. Also check out our

[email protected] for all sorts of additional content. See you next time. Finance for physicians is not an investment tax legal or financial advisor. All content included in this podcast is for informational purposes only and should not be considered financial tax or legal advice. Material presented. It is believed to be from reliable sources and no representations are made by finance for physicians as to another parties, informational accuracy or completeness, all information or ideas provided should be discussed in detail with an advisor accountant or legal counsel prior to implementation. You don't have an advisor or like a second opinion. Feel free to check out our website for recommended advisors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}